Volatility Refinery: BTC Capital Markets and Insurance Markets

This afternoon, I watched @PunterJeff’s outstanding RiskWorld keynote and was struck by how powerfully insurance markets provide a framework for understanding what companies like Strive and Strategy are building through Bitcoin, digital credit, and volatility structuring.

https://youtube.com/watch?v=18rFw-94wwE (Link to Full Presentation)

It turns out Insurance markets/reinsurance markets refine volatility & Bitcoin Capital Markets (MSTR/Strive) are doing the same thing with digital credit.

THAT'S INTERESTING!

Insurance markets are fundamentally risk allocation systems. They take unpredictable real-world volatility: fires, hurricanes, disasters then structure and redistribute that volatility to different capital layers: A useful framework for understanding Bitcoin, equity, and digital credit.

Start with a basic insurance company: Thousands of homeowners pay premiums every month. The insurer collects this steady cash flow “in the door” in exchange for taking on the risk that something bad happens later: Wildfire, Flood, Hurricane, Major loss.

This creates a business that looks stable…until catastrophe strikes.

Because the insurer does NOT know:

If a wildfire will happen, When it will happen, How severe it will be.

So beneath the steady premium flow is embedded volatility.

Insurance companies therefore do NOT usually want to keep all catastrophic volatility themselves.

Why?

Because one extreme event could overwhelm capital reserves.

So they “cede” or sell part of that tail risk to another layer:

REINSURANCE

Reinsurers are essentially insurers for insurance companies.

They say: “We will absorb some of your catastrophic volatility…but only if we are compensated appropriately.”

So insurers trade some upside (premium/profit) for greater stability.

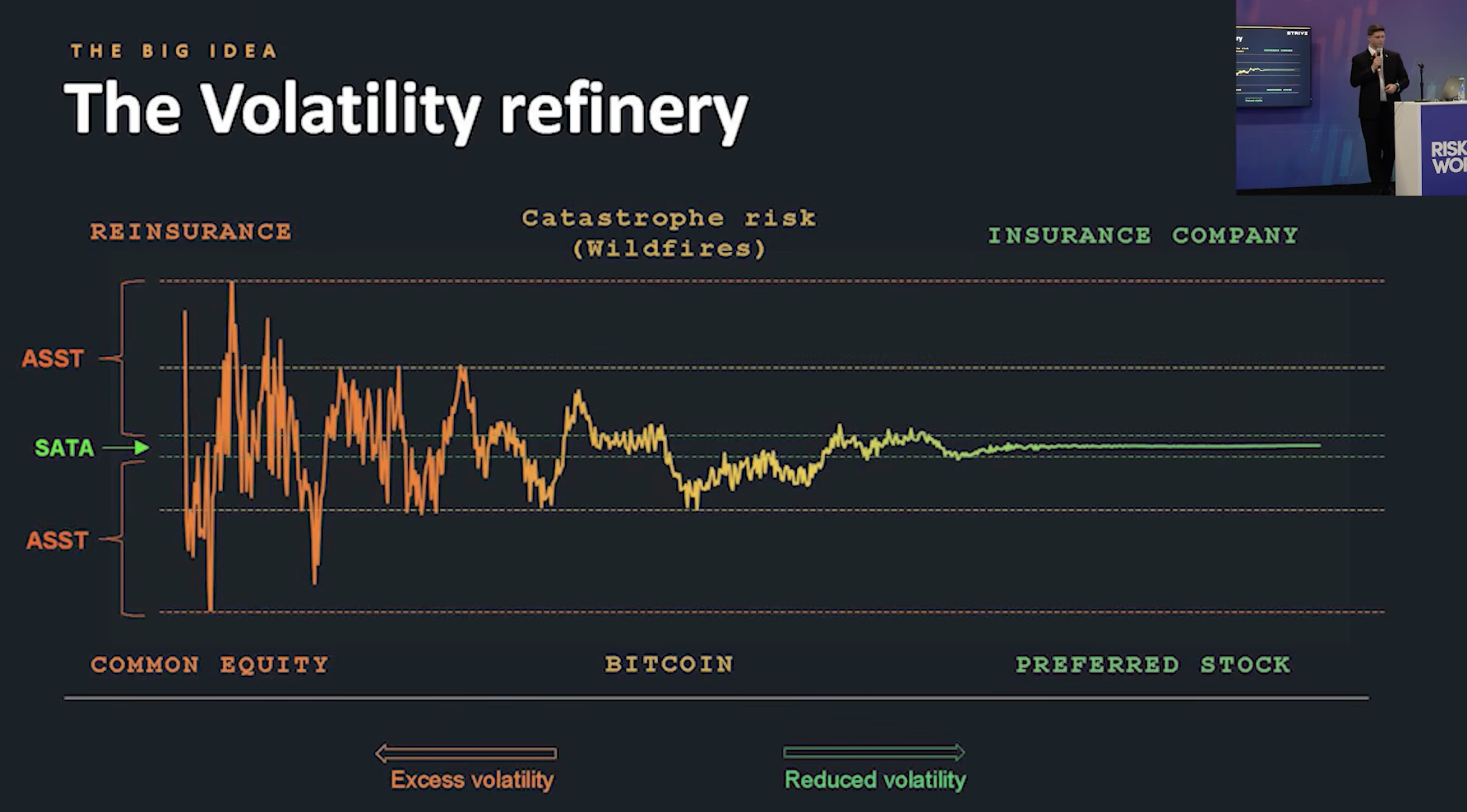

This creates layered risk allocation:

Homeowners → transfer risk to insurer Insurer → transfers tail risk to reinsurer

Result: Volatility is pushed upward to the capital willing to bear more uncertainty.

So, insurance company = lower volatility / steadier business / lower but more predictable returns.

Reinsurer = higher volatility / catastrophe absorber / higher potential returns

Reinsurance does NOT eliminate risk. It redistributes it.

This is the core function:

Volatility suppression through structured allocation

Now apply this to capital markets:

A volatile enterprise (Bitcoin, common equity, ASST) can also be “layered.”

Some investors want:

Stability + yield + priority. Others want: Higher volatility + more upside

This is where preferred stock / digital credit may resemble the insurance layer: Preferred / SATA:

Lower volatility, More predictable claim, Reduced upside, Capital protection focus.

Like insurers collecting steady premiums.

Meanwhile common equity / ASST may resemble the reinsurance layer: residual claimant absorbs more volatility, greater upside, greater downside tail-risk exposure.

Like reinsurers monetizing catastrophe.

So both industries are doing something very similar:

Insurance: Transforms catastrophe risk into structured financial layers.

BTC Capital markets: Transforms volatility from BTC into structured financial layers of various forms of equity.

Both are businesses of:

Risk allocation, Volatility suppression, Capital structuring.

Neither destroys volatility. They sort it.

Insurance scaled by learning how to package uncertainty.

Bitcoin-native capital markets are doing something similar… Structuring volatility for broader adoption.

And it seems to be just getting started.

Thanks for the lesson Jeff.