Reality Always Wins: Why Healthy Economies Must Stay Tethered To The Real World

“Money is a tool of exchange, which can't exist unless there are goods produced and men able

to produce them.”

— Ayn Rand, Atlas Shrugged

For more than fifty years, the developed world has enjoyed a remarkable privilege:

The ability to create financial claims far faster than it created the real-world production needed to support them.

Government debt, government spending, financial assets, asset prices all expanded and for decades, the system appeared to work.

But beneath the surface, a dangerous assumption was taking hold:

That financial claims could grow indefinitely while remaining detached from the physical economy upon which they ultimately depend.

Now, that assumption is now being tested, because eventually every economic system encounters the same constraint: Reality.

Reality cannot be printed, borrowed or legislated into existence.

Factories must still be built.

Energy must still be produced.

Commodities must still be mined.

Rare Earth Minerals must still be refined.

Food must still be grown.

And military power must still be supported by industrial capacity.

For a time, in the short term, debt can obscure these realities, but eventually reality enforces the truth.

In my previous article, “The Neutral Reserve Asset Theory: Gold, Bitcoin, and the Rise of an Alternative Deficit Structure”, I explored how China has begun experimenting with a trade-settlement framework that relies less on sovereign debt markets and more on neutral reserve assets such as gold.

This article explores a deeper question: Why might the world be moving in that direction in the first place?

The answer, I believe, is surprisingly simple and rooted in fundamental Austrian Economic Theory. Whether you are an individual, a company, or a nation, long-term economic health depends upon remaining tethered to reality, and throughout history, the monetary systems that endured the longest were often those anchored by assets that could not be created by political decree.

Assets that required time and energy and real world sacrifice to produce.

Assets that forced economic actors to confront reality rather than postpone it.

Today, as debt burdens reach historic extremes across much of the developed world, reality may once again be demanding a larger role in the monetary system.

And that may explain why Gold, and eventually Bitcoin, are becoming increasingly important.

The Purpose of Money

Before discussing debt, Gold, or Bitcoin, it is worth asking a more fundamental question:

What makes a good money?

Throughout history, societies have gravitated toward forms of money that share similar characteristics: They are scarce, durable, difficult to produce and widely recognized.

And most importantly, they require meaningful time, energy, capital, and sacrifice to create.

Money is not merely a medium of exchange - It is a measuring stick.

It is society's way of recording economic value across time and space.

Money is ultimately a claim on human time, energy, labor, resources, and production. For that claim to remain honest, the monetary units themselves must be difficult to create. Otherwise, the quantity of claims grows faster than the quantity of real-world wealth available to satisfy them.

For money to remain a useful measuring stick, the creation of new monetary units must stay tethered to the real-world production those units are meant to represent. A dollar is not valuable simply because it exists; it is valuable because it can reliably command goods, services, labor, energy, and time.

For example, if someone accepts $100 in exchange for an hour of their labor, they are trusting that those $100 will still map onto a meaningful amount of real-world value later. That value might be measured in food, fuel, shelter, or energy-intensive commodities like oil. But if the same $100 gradually commands less oil, fewer goods, or less human labor, then it is no longer preserving value across time and space.

At that point, the worker has not become more expensive. The money has become a less reliable claim on reality. So eventually, the worker demands more dollars for the same hour of time and energy.

When that relationship breaks down, distortions emerge, and this is where paper claims become problematic.

Unlike gold, oil, copper, farmland, factories, or skilled labor, paper claims can often be created with little or no corresponding expenditure of time, energy, or physical resources.

This creates a powerful temptation, as If claims can be created more easily than real wealth itself, those closest to the source of claim creation gain an enormous advantage.

This is not a moral indictment of any particular group - it is simply human nature - if individuals, institutions, or governments are given the ability to obtain something at little cost while receiving the benefits immediately, they will tend to do so.

And throughout history, nearly every society has struggled with this temptation.

It’s not that people are bad, it is that incentives matter, and good money is a profound tool for humanity precisely because it constrains those incentives.

It forces economic actors to expend real effort before acquiring additional monetary claims and in doing so, it helps tether the financial world to the physical world.Bad money, by contrast, allows this tether to weaken.

For a time, this can appear beneficial, as additional claims create spending power.

Asset prices rise.

Financial activity expands.

Economic pain can be postponed.

The future can be borrowed into the present.

But the postponement is never permanent as the underlying reality remains unchanged.

Factories must still produce.

Energy must still be generated.

Food must still be grown.

Rare Earth Minerals must still be refined.

Commodities must still be extracted.

Military equipment must still be manufactured.

Eventually, the quantity of claims must reconcile with the quantity of real-world production available to satisfy them.

Reality always performs the final audit.

And throughout history, the monetary systems that endured the longest were often those that made it hardest to escape that audit.

Once money becomes too easy to create, the economy gradually reorganizes around access to claim creation rather than real-world production.

And it is precisely this dynamic that helps explain the economic path the developed world has followed over the last half century.

The Triffin Trade

The United States Dollar acts as the global reserve currency, meaning that most trade and global debt is denominated in USD, and most of the worlds savings are stored in the form of US Government debt (aka Treasuries). The arrangement has allowed America to consume beyond its production, finance persistent deficits, and enjoy extraordinary fiscal flexibility.

But the arrangement carried a hidden dilemma.

The Triffin Dilemma is that to be the global reserve currency, means you have to run persistent trade deficits. To supply the world with dollars, America runs persistent trade deficits, meaning we import more goods and services than we export. This ensures that the world gets supplied with dollars, which they largely re-invest into US assets like Treasuries, increasingly supplying the world with US Government debt.

This keeps the USD artificially strong compared to other currencies due to a persistent global demand for dollars, and consequently makes US domestic manufacturing uncompetitive as foreign nations can produce with cheaper labor (as they can pay in “cheaper” local currencies).

As productive capacity gradually migrated overseas, this effectively “hollowed out” the US manufacturing base.

Industrial supply chains moved.Commodity processing moved.

Rare-earth refining moved.

And over time, America became extraordinarily skilled at producing financial assets while becoming less capable of producing many of the physical goods upon which those financial assets ultimately depend.

This structural reality enriched certain sectors: Wall Street flourished as they could create and sell more and more financial products.

Asset owners flourished, as foreign entities bought up more and more equities, real estate, and other US assets paid for with the dollars received for goods exported.

And Washington gained enormous spending flexibility, enriching all those politically connected.

But other sectors paid the price:

Manufacturing declined.

Industrial employment declined.

And engineering and production became relatively less rewarded than finance.

Increasingly, the nation's brightest minds were incentivized not to build physical systems, but to optimize capital structures and financial tools.

For decades, this seemed manageable, even “normal”, but recently we are seeing reality intervene.

Reality Arrives

Recent geopolitical conflicts have exposed a difficult truth:

Military power ultimately depends on industrial power.

Missiles require factories.

Semiconductors require supply chains.

Rare-earth minerals require processing capacity.

Energy security requires physical infrastructure.

Financial assets cannot manufacture artillery shells.

Treasury securities cannot produce missiles.

Bond portfolios cannot refine rare-earth metals.

When the war in Ukraine erupted, Western governments discovered that years of financial abundance had not translated into equivalent industrial readiness. Expanding artillery shell production required years of investment in factories, equipment, skilled labor, and logistics. By early 2023, the U.S. had sent Ukraine roughly one-third of its Javelin inventory and about one - quarter of its Stinger inventory, systems CSIS estimated would take years to replace. The same lesson emerged in rare earths, key materials that make up everything from computer chips to military weapons. China today dominates global rare-earth capacity, mining about 60–70% of the world’s RE’s but processing nearly 90% of them, giving it a chokehold on the most critical step in the supply chain. In doing so it can control much of the refining infrastructure essential to advanced electronics, renewable energy systems, and military hardware.

The lesson is simple:

You can print dollars but you cannot print industrial capacity.

The Sovereign Debt Trap

The same dynamic now appears in sovereign debt markets. For decades, governments financed deficits by issuing more debt.

The debt was absorbed and the system continued, albeit with persistently high inflation, and a bifurcating economy where wall street prospered while main street struggled.

Eventually, however, the debt itself has become the constraint, as higher debt requires higher issuance, and higher issuance pressures yields as more supply causes lower bond prices.

Higher yields increase interest expense, and higher interest expense creates larger deficits.

Larger deficits require still more issuance, and the system begins feeding on itself.

The mechanism that once created stability begins creating instability.

Consider the United States today:

Federal debt has risen to roughly 120% of GDP.

Annual interest expense (alone) is approaching $1 trillion.

For the first time in modern history, interest costs are rivaling some of the government's largest spending categories, including national defense.

The debt itself is becoming one of the largest line items in the federal budget.

Increasingly, bond market behavior is suggesting investors are becoming less concerned with

inflation alone and more concerned with fiscal sustainability or “default risk”.

Reality is once again asserting itself.

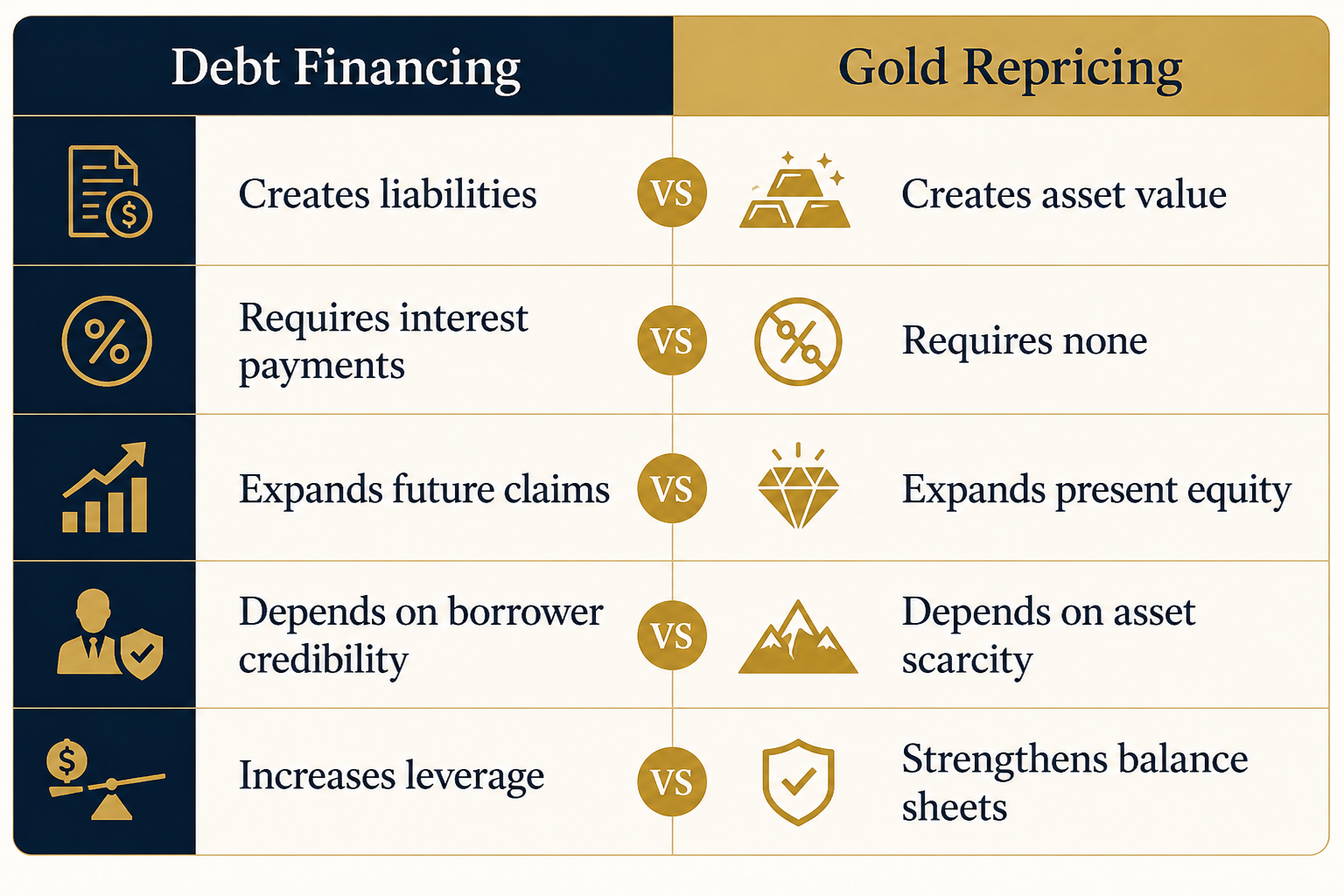

Debt Creates Claims. Gold Creates Equity

Most people assume deficits can only be financed through additional borrowing.

But there is another possibility - balance sheets can improve through asset revaluation.

This distinction is critical.

When governments issue debt, they create new obligations, but when reserve assets

appreciate, balance sheets strengthen without creating new liabilities.

One expands claims. The other expands equity.

Why Gold Matters

Gold is often misunderstood.

Its importance is not that it is shiny or that it is ancient.

Its importance is that it cannot be created through political decree.

Gold requires labor, energy, capital and time to create.

There are only two ways to get gold, to earn it from someone who has it, or to mine it. And

both require time and energy.

As such, every ounce represents the expenditure of real-world resources.

This makes gold fundamentally different from sovereign debt.

Debt can be created with a vote or a keystroke.

Debt is a claim

Debt expands through promises.

Gold is hard to produce

Gold is an asset

Gold expands through production.

Most importantly, gold is uniquely suited to absorb monetary imbalances as unlike oil, copper, food or industrial commodities, gold has relatively limited industrial utility.

A doubling in the price of gold does not meaningfully raise the cost of producing automobiles, semiconductors, electricity, or food, so Gold can absorb monetary demand without transmitting significant inflationary pressure throughout the productive economy.

In a sense, gold acts as a monetary sponge, it absorbs excess claims without requiring additional debt.

And because it is a bearer asset, neutral reserve asset, and nobody's liability, it can serve as a bridge between competing nations without requiring trust in a counterparty.

This is precisely what makes it so useful.

The Great Recapitalization

This is where the story becomes counterintuitive.

Many investors assume higher gold prices signal monetary failure, as this usually indicates lack of faith in the monetary system, but heavily indebted sovereigns may increasingly discover that higher gold prices may actually instill faith in their clearly fracturing currencies.

Higher gold prices strengthen sovereign balance sheets, as nation state central banks stockpile vast amounts of Gold bullion.

Thus higher gold prices increase the value of these reserves, giving strength back to the currencies and faith in the government debt. Higher gold prices also allow global imbalances to be absorbed through asset revaluation rather than additional debt issuance, for example if I’m importing $1m of oil, I could settle in (newly revalued) gold reserves rather than issuing fresh government debt in USD to pay for it.

Government debt that has all the accompanying liabilities and future payment responsibilities.

The scale of this is enormous. The United States officially holds more than 8,100 tonnes of gold.

Germany holds roughly 3,300 tonnes.

Italy holds roughly 2,450 tonnes.

France holds more than 2,400 tonnes.

Some of the world's most indebted nations continue to hold enormous gold reserves because gold remains one of the few reserve assets capable of strengthening sovereign balance sheets without creating additional liabilities.

In effect, gold offers a mechanism for recapitalization without requiring still more leverage.

The Market Is Already Voting

Whether policymakers fully recognize it or not, markets may already be moving in this direction.

Central-bank gold purchases have reached some of the highest levels on record and Gold has made repeated all-time highs across numerous currencies.

Long-term sovereign bond yields have risen globally despite slowing economic growth and China has steadily increased its gold reserves while reducing its relative dependence on U.S. Treasury assets. China is also settling more and more trade through the CNY (Yuan) which producers are taking and immediately converting to Gold through the many gold exchanges

China has set up across the world.

Taken together, these developments suggest a common theme:

The world may be searching for ways to settle imbalances without relying exclusively on ever-expanding debt markets.

The world is searching for a way back to reality.

Why Everyone Benefits

The beauty of the structure is that incentives begin to align.

Governments gain stronger balance sheets and commodity producers receive settlement in a neutral reserve asset.

Manufacturing economies gain incentives to rebuild productive capacity and investors benefit from ownership of scarce monetary assets.

The system becomes increasingly tied to production rather than leverage - increasingly tied to savings rather than consumption and reality rather than promises.

For the first time in decades, the interests of sovereigns, commodity producers, manufacturers, and holders of scarce monetary assets may be pointing in the same direction.

Toward higher gold prices.

Bitcoin: The Next Anchor

Gold may not be the final destination, but it may be the bridge towards a digital neutral reserve asset than doesn’t suffer from the physical constraints, frictions and costs of Gold.

Bitcoin shares the qualities that make gold valuable like scarcity, neutrality, bearer ownership and freedom from political control.

But Bitcoin introduces something entirely new - absolute supply certainty, perfect portability, near-instant global settlement and perfect verifiability.

Gold is scarce.

Bitcoin is absolutely scarce.

Gold requires trust in custody.

Bitcoin allows direct verification.

Gold can anchor a monetary system to reality.

Bitcoin may be capable of doing so even more precisely.

If the twentieth century was defined by sovereign debt as the world's settlement asset, and the twenty-first century increasingly reintroduces gold as a neutral reserve asset, Bitcoin may ultimately represent the next evolutionary step.

Not because it replaces reality, but because it measures reality more honestly.

Conclusion

For more than fifty years, debt allowed the future to be borrowed into the present and for many in this system, it generated enormous prosperity.

But it also generated enormous leverage.

Today, the developed world faces a simple problem:

The quantity of financial claims is growing faster than the productive economy capable of satisfying them and reality is beginning to matter again.

The era of solving every imbalance with additional debt may be drawing to a close as buyers of government debt no longer see the value in storing energy in paper claims that have no tether to real-world value.

These natural market forces are ushering in the next era defined not by more promises, but by a return to assets that are connected to time and physical energy.

Whenever reality reasserts itself (and it always will), scarce assets tend to matter more than claims.

That is why gold matters, and that will ultimately be why Bitcoin matters even more.