The Neutral Reserve Asset Theory: Gold, Bitcoin, and the Rise of an Alternative Deficit Structure

Inspired by a fascinating exchange between Luke Gromen and Sarcastic Hedgie, a deeper question emerges beneath the surface of trade deficits, reserve assets, and sovereign debt.

What if global trade imbalances no longer needed to be financed primarily through government debt markets?

What if they could instead be absorbed through the repricing of a scarce neutral reserve asset?

And perhaps most importantly:

What if this process is already underway?

The Traditional Dollar System

To understand the alternative, we first need to understand the existing structure.

Under the current dollar reserve system:

1. Exporter nations sell goods to deficit nations (primarily the United States)

2. Exporters receive dollars

3. Those dollars are recycled into U.S. Treasuries and dollar assets

4. The U.S. government issues debt liabilities in return

The mechanism is elegant in one sense:

America gets goods today in exchange for promises to pay later.

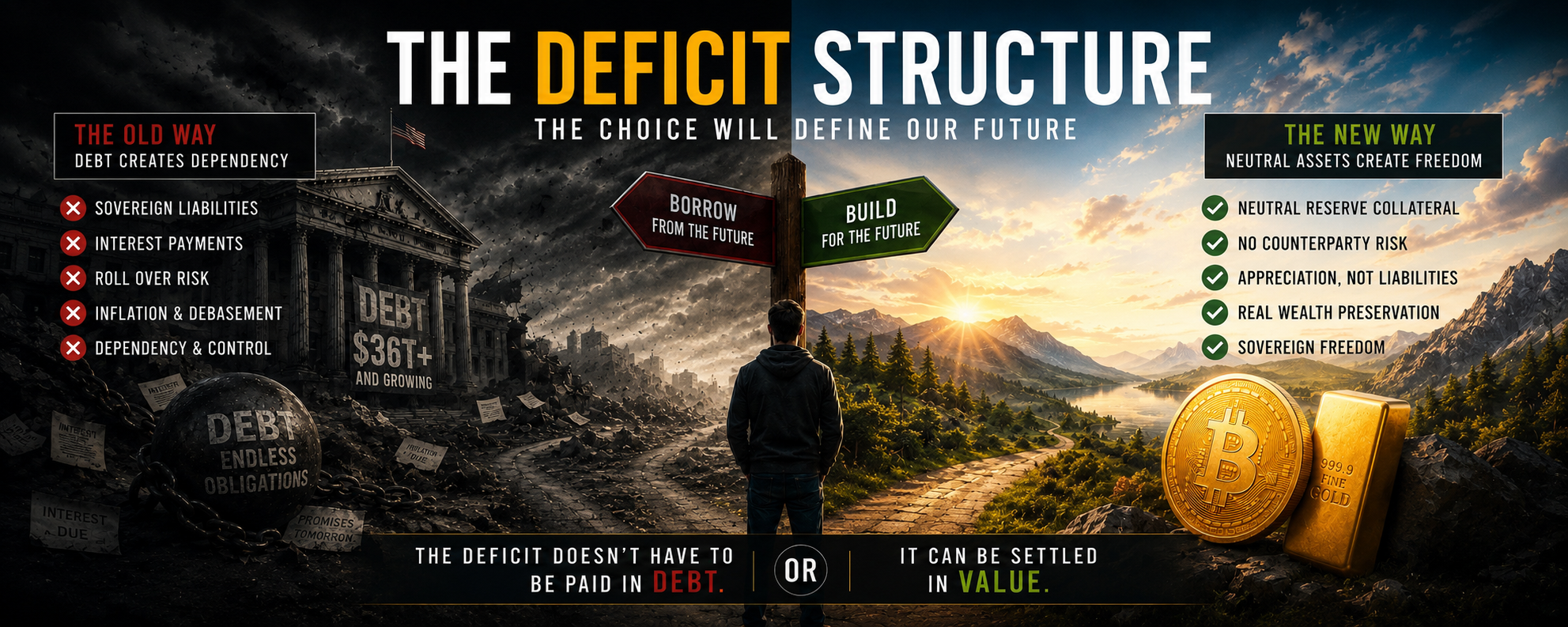

But structurally, this means global trade deficits:

* Expand sovereign liabilities

* Grow interest burdens

* Increase Treasury issuance

* Create perpetual rollover requirements

* Lead to fiscal dependence on low interest rates

The reserve system therefore depends not merely on trust in the dollar, but on continuous

demand for U.S. government debt itself.

The deficit is financed through liabilities.

The Treasury Recycling Machine

The post-Bretton Woods world effectively created a system where surplus nations

accumulated U.S. debt as reserve assets.

Oil exporters sold energy.

Manufacturing exporters sold goods.

Trade surpluses accumulated.

Then those surpluses flowed back into:

* Treasuries

* U.S. equities

* Real estate

* Other dollar-denominated claims

This arrangement benefited certain constituents in the United States enormously due to:

* Lower borrowing costs

* Stronger asset prices

* Cheaper financing

* The ability to sustain persistent current account deficits

So if you were the Washington elite, Wall Street, or the Top .01% (asset holders) you gained

disproportionately from this mechanism.

Politicians gained from having an essentially “blank check” of spending they could administer

(potentially to align themselves with certain interests and/or enrich close associates).

Wall Street benefited from a hyper financialized economy that requires money mangers, a

plethora of financial products/ services, and a continuous flood of new money into the financial

markets.

The top asset holders also benefited due to these currency flows consistently propping up real

estate, equities, and all scarce desirable goods.

But the tradeoff becomes obvious over time:

The larger the deficits become, the larger the sovereign debt structure required to support

them, as deficits require expanding liabilities.

An Alternative Structure

Now imagine a different arrangement.

Instead of trade imbalances being recycled primarily into sovereign debt, they are absorbed

through appreciation in a scarce reserve collateral asset.

Under this arrangement, the structure changes completely.

Alternative Reserve Asset System

Commodity exporter sells oil → receives currency → converts into scarce neutral reserve asset

→ asset appreciates in currency terms

Result:

* Exporter compensated

* But without requiring equivalent sovereign debt expansion

* No coupon payments

* No refinancing risk

* No maturity ladder

* No direct liability issued by the importing nation

In this framework, the reserve asset itself absorbs the imbalance.The deficit is financed through collateral appreciation rather than expanding debt issuance.

Why Gold Matters Again

This framework may help explain why gold has quietly become increasingly important

geopolitically.

Gold possesses several unique characteristics:

* No counterparty risk

* No sovereign issuer

* Globally recognized collateral

* Politically neutral

* Finite supply

* Thousands of years of monetary history

Critically:

Gold is not someone else’s liability.

Where a Treasury bond is an asset to the holder, it is simultaneously a liability of the U.S.

government.

But Gold is simply an asset.

That distinction matters immensely in a world increasingly concerned with sovereign debt

sustainability.

Is China Already Doing This?

This is where the Luke Gromen / Sarcastic Hedgie exchange becomes especially interesting.

China may increasingly be settling portions of its trade surplus not through accumulation of

additional Treasuries, but through:

* Gold accumulation

* Commodity control

* Reserve diversification

If gold appreciates substantially in yuan terms, China effectively monetizes trade surpluses

through balance sheet asset appreciation rather than solely through sovereign debt

accumulation.

In other words:

The reserve collateral rises in value instead of the debtor nation issuing ever-larger liabilities,

which is structurally much cleaner, as the creditor gets compensated but the compensation

mechanism does not require the debtor to endlessly compound debt obligations.

The Petrodollar Parallel

Sarcastic Hedgie referenced:“The cleanest deficit financing since oil-for-gold in the 70s”

That observation points toward an under-appreciated historical reality. After the collapse of

Bretton Woods in 1971, oil became deeply intertwined with dollar demand. Global energy trade

created persistent structural demand for dollars and Treasury recycling.

But today, another possibility may be emerging: a world where neutral reserve collateral, not

sovereign debt alone, absorbs trade imbalances.

Gold appears increasingly relevant within this framework, and eventually, another candidate

may emerge: Bitcoin.

Where Bitcoin Fits

Could Bitcoin one day serve a similar role?

Bitcoin shares many of gold’s monetary characteristics:

* Scarce

* Globally transferable

* Politically neutral

* Bearer asset

* Difficult to confiscate

* No sovereign liability attached

* Finite supply

If exporter nations eventually choose to hold Bitcoin rather than sovereign debt reserves, an

entirely new global settlement architecture could emerge.

Trade deficits could increasingly settle through reserve asset repricing, collateral appreciation,

and balance sheet reserve accumulation, rather than perpetual sovereign debt issuance.

This would represent a profound shift to a new asset class and a new deficit structure

altogether.

The Real Question

The deeper issue is not whether Gold or Bitcoin “replace the dollar.”

The more important question will be what asset best absorbs global imbalances in a world

increasingly saturated with sovereign debt?

Because every reserve system ultimately depends on:

* Trust

* Collateral

* Liquidity

* Balance sheet sustainability

And history suggests that when debt structures become too large, the world begins searching for neutral collateral once again.

It will be interesting to see how much capital moves to gold as a global natural reserve asset,

and as its market cap grows in size, how much increasingly moves to Bitcoin to take its place.