The New Sovereignty Stack: AI, Bitcoin, and the Compounding Advantage of Leverage

The New Sovereignty Stack

AI, Bitcoin, and the Compounding Advantage of Leverage

The modern economy is not merely divided between rich and poor. It is divided between those

with access to compounding leverage and those without it.

In the fiat system, that leverage comes through proximity to newly created money, asset

ownership, collateral, and credit. Those who own scarce assets can borrow against them,

acquire more assets, and watch monetary debasement push the value of those assets higher

over time. Those without assets are left trying to save depreciating currency fast enough to buy

into a market that, like an accelerating treadmill, keeps moving away from them.

As that divide intensifies, another divide is emerging.

Artificial intelligence introduces a different kind of leverage: cognitive leverage. It allows

individuals to research, write, design, code, analyze, synthesize, prototype, publish, and create

at a speed that would have been impossible only a few years ago. In allowing creators to more

easily bring their visions to life, it compresses the distance between idea and execution.

This does not mean AI will make everyone brilliant - It will not. In fact, AI may do the opposite,

as for those who use it passively, it may weaken judgment, flatten thinking, and reward

dependence.

But for high-agency people with taste, curiosity, independent judgment, courage, creativity,

and the willingness to fail, AI will become a compounding engine that creates a leverage loop

that drives incredible value to digital creators.

The key understanding is the degree to which AI changes the landscape of executing an idea.

The scarce resource is no longer productive capability, it is judgment, taste, creativity, courage,

and the ability to ask better questions.

And Bitcoin is the bridge between these two worlds: the fiat world of financial leverage and the

AI world of cognitive leverage. Bitcoin gives individuals access to scarce, divisible, globally

liquid collateral and AI gives individuals a production engine. Together, they form a new

sovereignty stack for the individual.

Part I: The Fiat Cantillon Loop

The Cantillon effect is the idea that newly created money does not enter the economy evenly.

New money does not fall equally from the sky. It enters through specific channels:

governments, banks, financial markets, large corporations, asset owners, and creditworthy

borrowers.

Those closest to the source of new money receive purchasing power before prices fully adjust.

Those farther away receive the effects later, often in the form of higher prices.

This matters because the early recipients of newly created money or credit can buy assets

before the broader market has repriced. They can acquire real estate, equities, businesses,

commodities, or other scarce assets before the inflationary effect has fully moved through the system.

Then, as new money continues to circulate, asset prices rise, so those who already owned

assets become wealthier.

Then something even more powerful happens: those assets become collateral.

This is the hidden lever of the Fiat system:

In a financialized economy, wealth is not only about income. It is about collateral.

The asset owner does not merely have a higher net worth. The asset owner has access to a

balance-sheet engine.

They can say:

I own appreciating collateral. I can borrow against it, buy more assets, and let inflation reduce

the real burden of my debt over time.

However, the non-asset holder is forced to play a different game:

I must earn income, save after tax, and hope asset prices do not rise faster than my savings

rate.

That is not the same game.

One person uses appreciating assets to access credit, while the other sells time for wages and

tries to save in the depreciating currency.

This is why the system feels increasingly impossible for many people lower on the ladder. They

are not merely behind - they lack access to the core compounding mechanism.

Imagine two people in 2012.

One owns a home and a stock portfolio. The other earns wages and holds cash.

After a decade of monetary expansion and asset inflation, the first person’s assets become

more valuable, which improves their borrowing power. They can refinance, borrow, invest, or

acquire more assets. The second person’s wages may rise, but the house they hoped to buy

rises faster. One person’s balance sheet compounds while the other person’s savings goal

moves away.

This is the brutal asymmetry of Fiat.

A homeowner with $500,000 of equity can borrow against that equity. A renter with the same

income but no collateral cannot access the same leverage.

The asset owner is not just wealthier, they are plugged into the compounding engine.

Moreover, the more leveraged someone becomes, the more trapped they are inside the

system, because their survival increasingly depends on that system continuing exactly as it is.

Over time, people become defenders of the very machine that is eroding their purchasing

power, mistaking asset inflation for prosperity while the real foundation beneath them grows

more fragile.

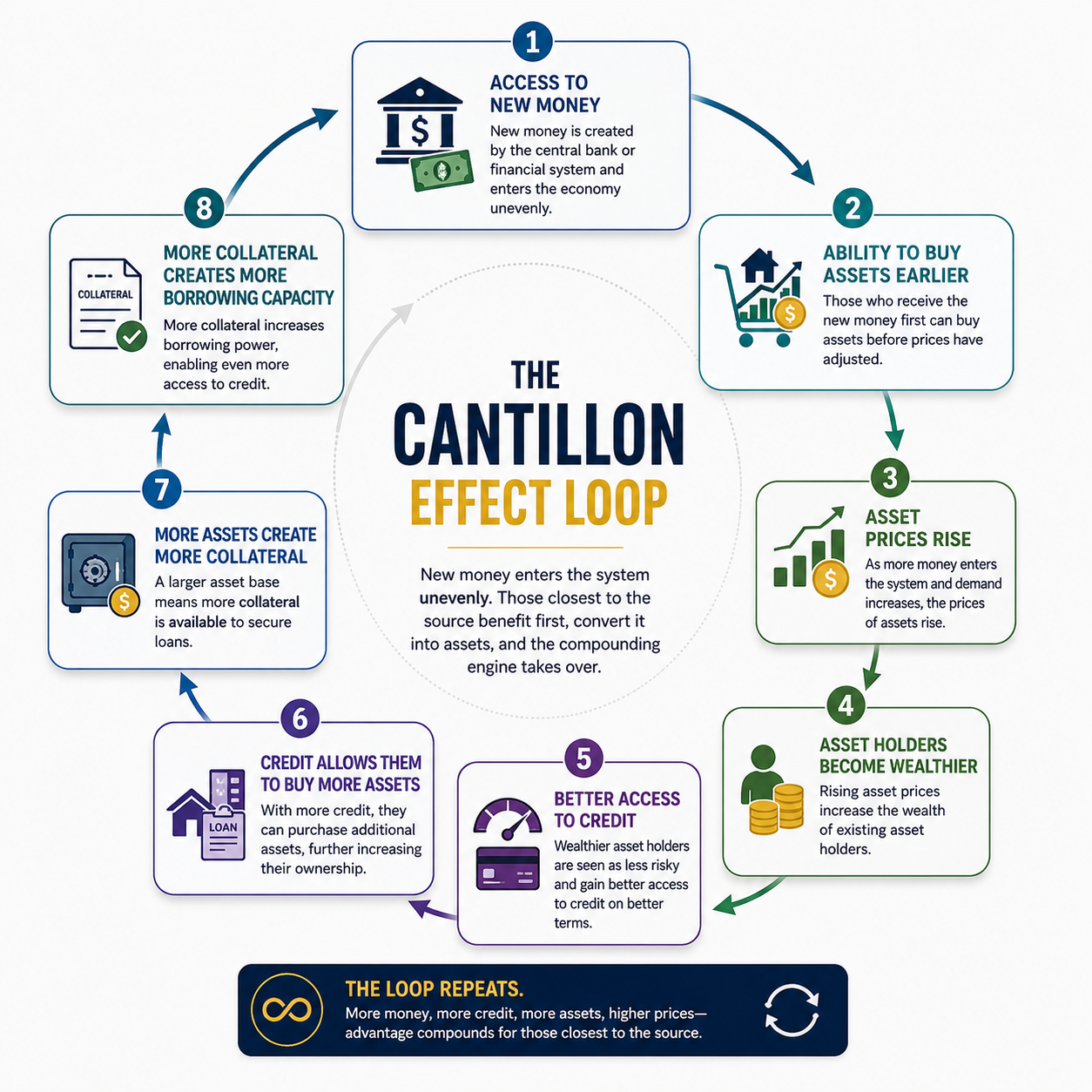

The fiat loop looks like this:

Access to new money

→ ability to buy assets earlier

→ asset prices rise

→ asset holders become wealthier

→ wealthier asset holders gain better access to credit

→ credit allows them to buy more assets

→ more assets create more collateral

→ more collateral creates more borrowing capacity

→ the loop repeats.

This is the reflexive engine of the asset class.

The rich get richer not merely because they have more money, but because the monetary

system rewards those who already own collateral, and money printing intensifies this divide.

In a fiat economic system like we have today, there is no “peg” “or backing” of the dollar to any

hard asset. In 1971, President Nixon famously took the US dollar off the gold standard by

making dollars no longer redeemable for gold. Before this moment, dollars could be redeemed

for gold and so gold acted as a “peg” or natural “limit” to the dollars expansion. With this peg,

the government could not print more dollars than they had in reserves (or there would be a

rush of redemptions, often called a “bank run”). This kept government spending in check and

dollar currency strength. However, in a fiat system where the dollar is backed by nothing

(except “faith” in the US Government) the money supply can expand, deficits can be financed,

and central banks can intervene to stabilize financial markets by creating more dollars.

In this world, asset prices often become the release valve for new liquidity, as dollars rush to

find the places where they will be treated best over time - scarce, desirable assets like stocks

and real estate.

If you already own assets, monetary expansion will lift your balance sheet. But if you do not

own assets, monetary expansion can raise the price of the very things you are trying to buy.

For the asset holder, inflation can be a tailwind, but for the wage earner, inflation is often a

hurdle.

And so society bifurcates.

On one side are those who own scarce assets and can use those assets as collateral, and on

the other side are those trying to save enough depreciating currency to acquire them.

This is the fiat divide.

It is not simply a divide between rich and poor. It is a divide between those who can access

compounding financial leverage and those who cannot: asset holders and everyone else.

Part II - The AI Advantage Loop

AI may be creating a similar reflexive loop in a different domain.

Not because AI is money, but because AI, like capital, is leverage.

In the fiat system, capital gives asset owners more power to acquire more capital. In the AI

system, cognitive leverage gives high-agency creators more power to create better outputs,

gain more attention, generate more revenue, acquire better tools, and improve their outputs

again.

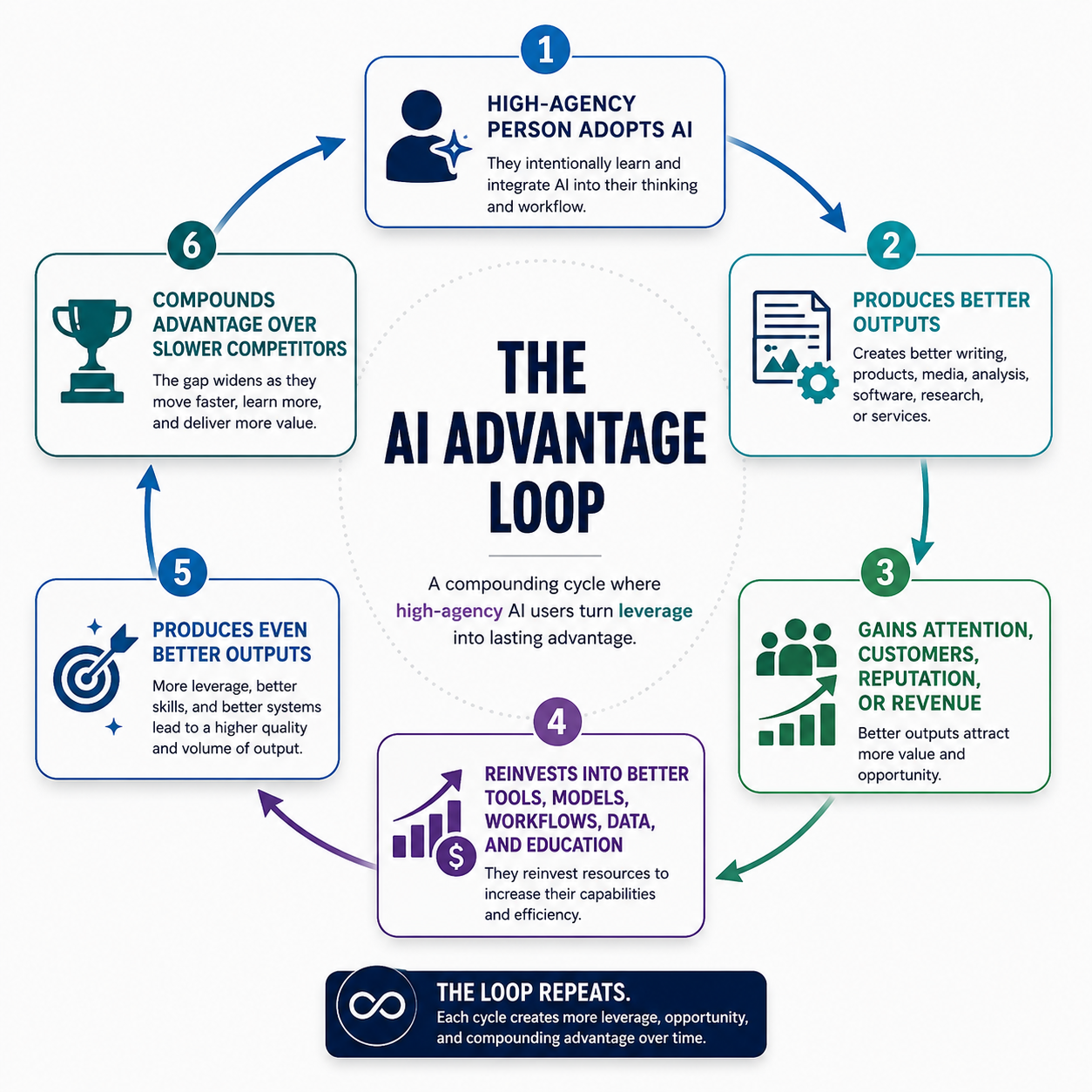

The AI loop looks like this:

High-agency person adopts AI

→ produces better writing, products, media, analysis, software, research, or services

→ gains attention, customers, reputation, or revenue

→ reinvests into better tools, models, workflows, data, and education

→ produces even better outputs

→ compounds advantage over slower competitors

→ the loop repeats.

That is the parallel: both systems reward those closest to the source of leverage.

In fiat, those closest to newly created money gain purchasing power before others. In AI, those

closest to frontier tools and best workflows gain productive capacity before others.

In both cases, an early advantage can compound.

Better tools produce better outputs. Better outputs attract attention, customers, revenue, or

reputation. Those resources can be reinvested into better tools, better systems, better

collaborators, better data, and better distribution and over time, the gap widens.

But there is an important distinction:

The Fiat Cantillon loop is largely about proximity to money creation, asset ownership,

institutional position, and credit access. Whereas the AI loop is more open and egalitarian as

its accessible to everyone with a computer and internet.

The ability to create value from AI is determined not by privilege, but by agency, skill, taste,

curiosity, creativity, and willingness to learn.

This difference matters because while Fiat compounds advantage through access to capital, AI

compounds advantage through access to cognitive leverage.

In the fiat system, those without assets are priced out of the future, but in the new world of AI,

it will be those without agency that are produced out of the future.

The legacy financial economy rewarded access to capital.

The new digital economy will reward judgement and agency.

Part III: The AI Divide

AI will not simply divide blue collar from white collar, because within white collar jobs, AI will

divide further, routine work from judgment work.

The first wave of disruption will hit routinized knowledge work hardest: paralegal document

review, entry-level accounting, junior financial analysis, clerical operations, administrative

healthcare work, customer service, marketing copy, basic research, compliance paperwork,

routine legal drafting, scheduling, and back-office coordination.

These are not necessarily “thinking” jobs in the deepest sense. They are often information-

processing jobs: searching, summarizing, formatting, drafting, reconciling, comparing,

organizing, and moving information from one place to another.

Because AI is very good at that, real question is not whether AI replaces a category of worker,

but whether a person uses AI to become more capable.

AI will not replace thinking. It will reveal who was thinking.

AI means that access to immense productive capability is democratized to everyone with a

computer, but mastery of that power is not. The internet gave everyone access to information,

but it did not make everyone wise. Social media gave everyone access to distribution, but it

did not make everyone influential. AI gives everyone access to production capacity, but it will

not make everyone creative, discerning, or brave.

That is the key distinction.

AI does not automatically make someone brilliant, but it will amplify the operator.

Part IV: The AI Divide Within

AI will make it easier than ever to produce words, images, videos, code, strategies, and

analysis. But easier production does not mean better production. In fact, the default output of

AI in the hands of a passive user may simply be more noise.

This is why judgment becomes more valuable, not less.

When everyone can generate 100 ideas, the scarce skill becomes knowing which three matter.

When everyone can produce content, the scarce skill becomes knowing what is worth saying.

When everyone can ask AI for an answer, the scarce skill becomes knowing which questions

are worth asking.

The first AI divide was obvious: those who use AI versus those who do not.

But the second divide may matter more:

Those who use AI to strengthen their thinking versus those who use AI to replace it.

Some people will use AI as a cognitive exoskeleton to refine ideas, run simulations and learn

areas of study with greater nuance. But many will use it as a cognitive crutch.

The high-agency user uses AI to sharpen ideas, test arguments, expose weak logic, generate

variations, explore counterarguments, build prototypes, improve writing, create visuals, speed

up learning, and ask better questions.

For this person, AI does not replace thinking, but increases the surface area of thinking.

But the low-agency user uses AI to avoid effort, summarize instead of understand, generate

answers instead of wrestling with questions, produce generic content, bypass learning,

outsource judgment, consume endless novelty, and ask the machine what to think.

For this person, AI may weaken the very faculties they need most to survive in the new world:

judgment, creativity, independent thought, patience, memory, and taste.

That is the danger.

The most important AI divide may not be between people who use AI and people who do not.

It may be between people who use AI to become more capable and people who use AI to

become more dependent.

Leverage cuts both ways:

In the hands of a builder, AI compounds creativity.

In the hands of a passive consumer, AI compounds dependency.

Part V: AI in the Lineage of Agency-Expanding Technologies

AI belongs in a long lineage of technologies that increased individual agency by collapsing

bottlenecks.

When Johannes Gutenberg developed the printing press in 1450, it did not make everyone

Shakespeare. But it did break the monopoly on written knowledge. Before the printing press,

knowledge was bottlenecked by scribes, churches, universities, and elite institutions. The

printing press massively reduced the cost of reproducing ideas. It enabled mass literacy,

religious reform, scientific communication, political pamphlets, individual interpretation of texts,

and the weakening of centralized information monopolies.

The printing press democratized knowledge.

The telegraph collapsed how fast information can travel across the globe. Before the telegraph,

information traveled at the speed of horse, ship, or human messenger. After it, prices, news,

military orders, and political messages could move almost instantly.

The telegraph democratized the speed of communication.

The internet did something even more dramatic. It did not make everyone a great entrepreneur,

writer, or thinker. But it broke the monopoly on distribution. A person no longer needed a

newspaper, publisher, TV network, record label, university, or corporate gatekeeper to reach

the world.

The internet democratized distribution.

Bitcoin challenges monetary monopolies. It enables counterfeit resistant savings, self-custody,

global value transfer, digital scarcity, and monetary exit from monies that only exist with the

permission of a centralized authority.

Bitcoin democratizes money.

AI is the next step in this evolution of technologies that grants agency and freedom to the

individual. AI does not merely distribute information, it helps produce, synthesize, analyze,

design, write, code, reason, and create.

AI is democratizing execution.

For most of history, there was a gap between what someone could imagine and what they

could produce, but AI collapses this gap. Before it, one might have had an idea for a book,

app, video, course, cartoon, investment memo, brand, or business, but production was

prohibitively expensive. Designers, editors, developers, researchers, assistants, agencies,

animators, analysts with years of technical skills and experience were needed. AI now

routinely take the place of these experts and is doing it increasingly better everyday.

We are moving from a world where people are limited by what they can produce to a world

where they are limited by what they can conceive.

But the winners will not merely be people with ideas. They will be people who can generate

ideas, distinguish good ones from bad ones, rapidly test them, refine them, ship them, learn

from feedback, and repeat.

The future may not belong to the person who works the longest hours. It may belong to the

person who can conceive most clearly, test most rapidly, and refine most intelligently.

AI does not eliminate work - It changes the nature of work.

The old economy of the factory worker, or 9-5 corporate office manager rewarded labor hours.

But the new economy will increasingly reward agency, judgment, and the ability to turn ideas

into reality.

Part VI: The Bitcoin Sovereignty Loop

Bitcoin is the bridge between the fiat leverage loop and the AI leverage loop.

In the legacy fiat system, financial leverage primarily belonged to those who already owned

assets. If one owned real estate, stocks, businesses, or other valuable assets, one could

borrow against them. One could use collateral to access credit. One could use credit to buy

more assets, and so one could participate in the compounding loop.

But the entry ticket was high.

A house is not easily divisible. A private business is not easily liquid. A Van Gogh painting

cannot be broken into small units by ordinary people and used as collateral. Commercial real

estate requires large amounts of capital and banking access.

Bitcoin is different.

Bitcoin is divisible, liquid, scarce, portable, global, and permissionless.

Someone can buy $50 worth, $500 worth, $5,000 worth, or $5 million worth. They do not need

to buy an entire house, an entire business, or an entire work of art to begin owning scarce

collateral.

This is profound because the fiat system rewards collateral ownership more than labor alone.

In democratizing money, Bitcoin also democratized access to the Fiat leverage loop, giving

ordinary people access to a starter form of pristine collateral. It democratized access to the

collateral game before people are permanently priced out of it.

Bitcoin gives ordinary people access to scarce, liquid collateral without needing prior access to

banks, real estate, or institutional credit. It offers the power of compounding leverage to

anyone with an iPhone, and also gives individuals access to an asset that can be accumulated

at any scale and used as a long-term capital base.

The point is not that leverage is automatically good, as we have seen earlier, leverage cuts both

ways. The point is that Bitcoin gives individuals access to a form of collateral that was

previously difficult to acquire at small scale, and allows them the same access to compounding

leverage on scarce, desirable assets that was previously only available to the privileged asset

class.

Part VII: Bitcoin as Monetary Escape Valve

In time, Bitcoin may also weaken the need for the Cantillon loop entirely.

In a fiat system, people know cash is melting. So they store monetary premium in anything they

believe will protect purchasing power: houses, stocks, land, art, watches, commodities,

collectibles, private businesses.

The problem with this is that many of these assets also have real utility value.

A house is for living.

Stocks represent productive businesses.

Commodities have industrial use.

So when these assets absorb excessive monetary premium, their prices become distorted.

This is most obvious in housing. When houses become financialized stores of value, families

are forced to compete not only with other families, but with investors, funds, foreign capital,

leverage, and monetary debasement.

The result is socially destructive - the home becomes less of a shelter and more of a monetary

asset.

Bitcoin offers a cleaner outlet because Bitcoin’s value is completely monetary. It has no

“intrinsic” worth - It does not need to be lived in, eaten, built with, or industrially consumed.

And this feature makes it an excellent money.

If the excess monetary premium from these other assets can flow into Bitcoin, it may reduce

the need for homes, stocks, commodities, art, and other utility-bearing assets to serve as

desperate inflation hedges, and bring their prices down closer to their “utility value”.

The Austrian (from “Austrian Economics”) argument is simple:

Money should be money so houses can be homes, equities can be businesses, and

commodities can be inputs.

If Bitcoin succeeds as a global store of value, then other assets may lose some of their

monetary premium. Houses may trade more on their utility as shelter. Stocks may trade more

on future cash flows. Commodities may trade more on industrial demand. Capital allocation

may become more honest.

This does not mean houses or stocks collapse. It means their prices may become less

distorted by the desperate need to escape currency debasement.

Bitcoin absorbs the monetary premium that fiat forced into everything else.

That is its deeper social function.

Bitcoin is both a way to participate in the collateral loop, and a way to escape the rigged fiat

version of that loop.

Part VIII: The Sovereignty Stack: AI Produces, Bitcoin Preserves

This is where Bitcoin and AI become most interesting together.

AI and Bitcoin are not the same kind of leverage: AI is a tool for production, whereas Bitcoin is

a tool for preservation.

One expands what an individual can create, while the other protects what an individual has

earned.

The current financial system gives leverage mainly to asset owners, but the new system will

give leverage to individuals through two channels:

Bitcoin: Financial leverage, savings, collateral, monetary escape.

AI: Cognitive leverage, production, creativity, execution.

Together, they form an individual sovereignty stack:

Bitcoin protects and collateralizes the value you accumulate.

AI helps you create value at higher speed and scale.

AI gives the individual a production engine while Bitcoin gives the individual a balance sheet.

Now a high-agency person can use AI to produce better products, services, media, research,

software, analysis, writing, and businesses. They can earn income, reputation, customers,

audience, or revenue. They can then store the fruits of that production in Bitcoin, an asset not

issued by a government, bank, or corporation, and they can access the power of compound

leverage in the same way that only wealthy elite were uniquely positioned for.

This creates a third loop:

Individuals acquire scarce digital collateral

→ Bitcoin offers a long-term alternative to saving in depreciating fiat

→ Bitcoin can become a long-term capital base

→ individuals gain access to capital without relying entirely on wage savings or institutional

proximity

→ Bitcoin absorbs monetary premium from distorted assets

→ advantage becomes more accessible

→ the loop repeats.

That is the Bitcoin Sovereignty Loop.

Part IX: The New Compounding Divide

The financial economy rewards access to capital, but the new digital economy will increasingly

reward the ability for creators to leverage their agency.

Either way, the deeper theme is the same:

Leverage compounds.

In the fiat system, leverage compounds around asset owners through money creation,

collateral, and credit.

In the AI system, leverage compounds around high-agency individuals who can turn ideas into

outputs at unprecedented speed.

In the Bitcoin system, leverage becomes more accessible because individuals can acquire

scarce, divisible collateral and store value in money that is not someone else’s liability.

These three loops explain the transition:

Loop 1: The Fiat Cantillon Loop

New money enters unevenly. Early recipients buy assets. Assets rise. Assets become collateral.

Collateral creates borrowing power. Borrowing power buys more assets. Advantage

compounds.

Loop 2: The AI Advantage Loop

High-agency people adopt AI. They produce better outputs. Better outputs create attention,

revenue, and reputation. They reinvest into better tools. Advantage compounds.

Loop 3: The Bitcoin Sovereignty Loop

Individuals acquire scarce digital collateral. Bitcoin offers monetary escape from fiat

debasement. It becomes a long-term balance-sheet asset and absorbs monetary premium

from distorted assets. Advantage becomes more accessible and compounds.

The important point is not that neither Bitcoin nor AI guarantees success -

The important point is that Bitcoin and AI increase agency and freedom for the individual and

remove the barriers to entry of these compounding loops. Loops that would otherwise be

protected or “walled” to only the privileged or entitled.

The person who uses AI to avoid thinking will not compound in the same way as the person

who uses AI to think better.

In the same way, the person who uses Bitcoin as a speculative casino chip will not benefit in

the same way as the person who uses Bitcoin as long-term savings and sovereign collateral.

Remember that leverage cuts both ways. The person who receives leverage without discipline

will destroy themselves, but the person who combines leverage with judgment can compound.

In the hands of individuals with agency, Bitcoin and AI will usher in a freedom and flourishing

humanity has never previously been equipped to experience.

Part X: Conclusion - Who Gets the Leverage?

The broad landscape of the economic system we are moving towards is that:

Fiat will continue to compounds advantage through asset ownership

AI will increasingly compound advantage through cognitive leverage

And

Bitcoin will democratize the collateral and protect the value individuals create.

This is the picture of the new world, as we integrate the latest agency and freedom technology

with the legacy system.

Fiat creates dependency by forcing people to chase assets simply to outrun debasement.

AI creates leverage because people can turn ideas into outputs without the barriers of the past.

Bitcoin creates sovereignty because people can store the fruits of that output in money that is

not someone else’s liability.

The future divide will not simply be rich versus poor, white collar versus blue collar, or AI users

versus non-AI users. It will be between those who control compounding engines and those

who do not.

Bitcoin gives individuals the balance sheet.

AI gives individuals the production engine.

The question is no longer merely who owns the assets - it is who controls the compounding

engines. Fiat gave that engine to the asset owner, and AI gives it to the builder, while Bitcoin

gives the builder a balance sheet.

And that is the new sovereignty stack.